Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

There was a period — let’s call it the Shoebox Era — when my entire bookkeeping system consisted of a spreadsheet named IMPORTANT_FINAL_v3_ACTUALFINAL.xlsx, a rubber-banded stack of receipts fading in the sun on my dashboard, and a business bank account that had, on more than one occasion, quietly paid for my dog’s vet bill. I found out I owed real, actual money to the IRS roughly eleven minutes before I found out I was two months behind on categorizing anything at all. Character-building? Sure. Necessary? Absolutely not.

If any of that sounds familiar, you’re not bad at business — you just haven’t built a system yet. So what does a bookkeeping system that actually works look like, and how much of it can you realistically run yourself? Let’s find out.

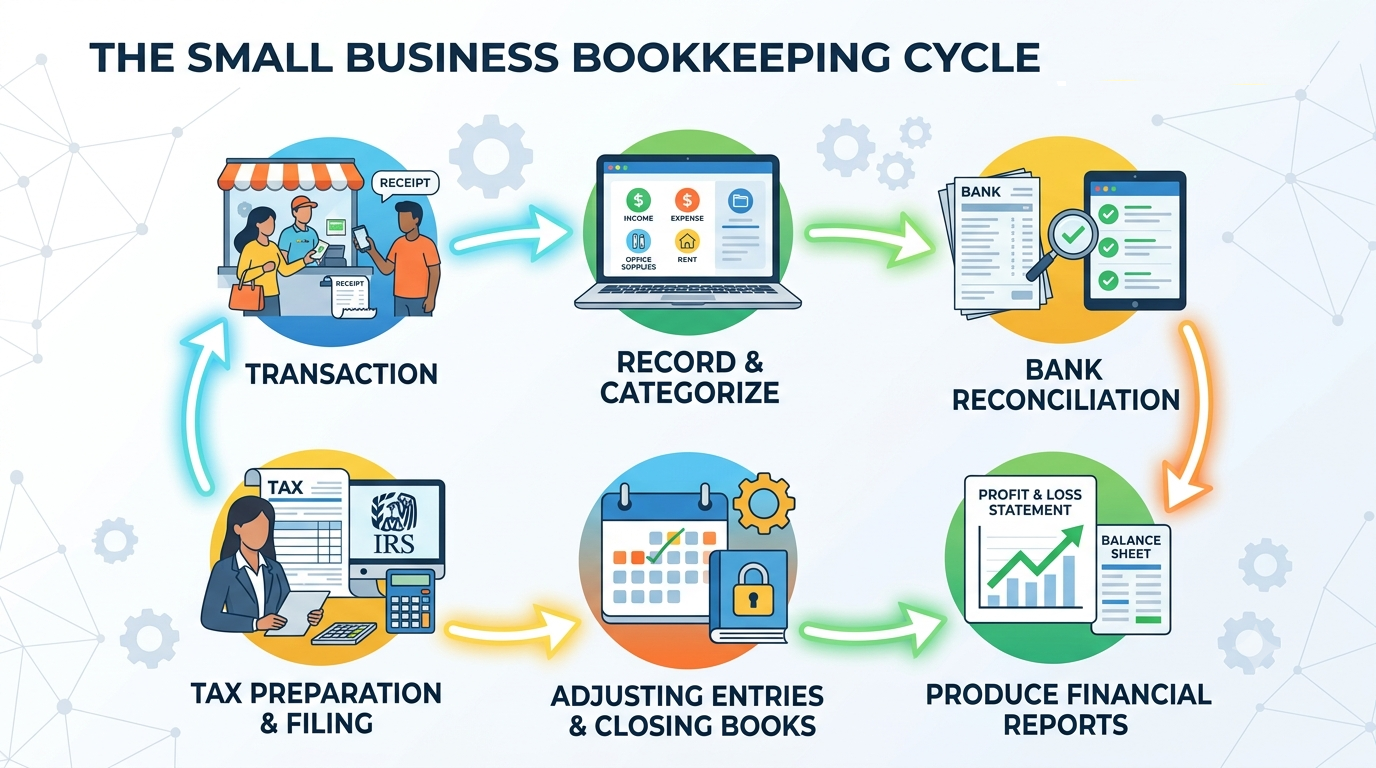

Bookkeeping for small business is the ongoing process of recording, organizing, and categorizing every financial transaction a company makes — sales, expenses, payroll, and beyond — to produce accurate records for tax filing, cash flow tracking, and informed decision-making. Done consistently, it turns a shoebox of receipts into a real-time picture of how your business is actually doing.

People use these words interchangeably, which is a bit like confusing the person who logs your grocery receipts with the person who tells you whether you can afford to eat out this month. Related jobs. Very different altitudes.

| Bookkeeping | Accounting | |

|---|---|---|

| Focus | Recording day-to-day transactions | Interpreting and analyzing financial data |

| Timeframe | Present — what happened today/this week | Big picture — trends, forecasts, strategy |

| Typical tasks | Categorizing expenses, invoicing, reconciling accounts | Preparing financial statements, tax strategy, advising on decisions |

| Who does it | You, an employee, or a bookkeeper | A CPA or accountant (often building on bookkeeping records) |

Good bookkeeping is what makes good accounting possible. Skip the first and the second one is just guessing with better vocabulary.

Before you record a single transaction, you need to pick an accounting method — it determines when income and expenses actually count.

| Cash Basis | Accrual Basis | |

|---|---|---|

| When revenue is recorded | When cash is received | When it’s earned (invoice sent), regardless of payment |

| When expenses are recorded | When cash leaves your account | When the expense is incurred, regardless of payment |

| Complexity | Simple, intuitive | More involved, needs more diligent tracking |

| Best for | Freelancers, solopreneurs, service businesses without inventory | Businesses with inventory, receivables, or that want a more accurate real-time financial picture |

| IRS note | Available to most businesses under $30M in average gross receipts (check current threshold) | Required for larger businesses and those carrying inventory |

If you’re a one-person consultancy invoicing a handful of clients, cash basis will probably feel more intuitive and require less bookkeeping overhead. If you’re holding inventory, extending credit to customers, or want financial statements that actually reflect your business’s health at a glance rather than just your bank balance, accrual is worth the extra structure.

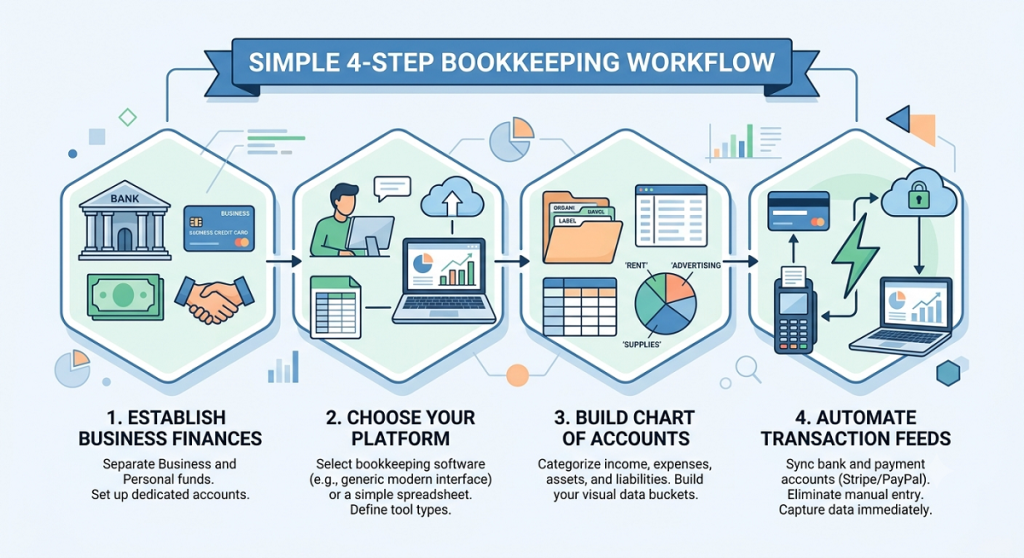

Four foundational steps, done once, save you from redoing everything later.

This is non-negotiable, and not just because it looks more professional. Mixing personal and business funds — commonly called “commingling” — makes every subsequent bookkeeping task harder, muddies your legal liability protection if you’re an LLC, and turns tax season into forensic archaeology.

A spreadsheet can work for the first few months of a very simple business. But most modern bookkeeping software pays for itself by automatically syncing bank and card transactions, auto-categorizing recurring expenses, and exporting tax-ready reports — the kind of manual work that eats hours every month if you’re doing it by hand. QuickBooks and Xero remain the most widely used general-purpose options, with a growing field of leaner, cheaper alternatives built specifically for solo and micro businesses.

Your chart of accounts is the categorized list of buckets — income, expenses, assets, liabilities, equity — that every transaction gets sorted into. Most software gives you a generic template to start from, but it’s worth tailoring it to your actual business. A construction company needs job-costing categories; a service business needs to separate subcontractor costs from software subscriptions. Set it up thoughtfully once, and every report you pull later will actually mean something.

Connect your bank accounts, credit cards, and payment processors (Stripe, PayPal, Square) directly to your bookkeeping software so transactions import automatically instead of requiring manual entry. Manual entry isn’t just tedious — it’s the single fastest way to fall behind, because it’s the first task that gets skipped when you’re busy.

Consistency beats intensity here. A little bit weekly prevents a lot of pain quarterly.

Weekly tasks

Monthly tasks

Quarterly and annual tasks

If you’re self-employed or otherwise responsible for quarterly estimated taxes in the U.S., the 2026 federal due dates are April 15, June 15, and September 15, 2026, with the fourth-quarter payment due January 15, 2027 — generally owed if you expect to owe $1,000 or more in federal tax for the year. Penalties are avoidable by paying at least 90% of the current year’s tax, or 100% of the prior year’s tax (110% if you’re a higher earner).

Bookkeeping produces data. These three reports are what turn that data into decisions.

Also called an income statement, this shows revenue minus expenses over a given period — the report that answers “am I actually making money?” Review it monthly, not just at tax time, so you catch a problem while it’s still small.

A snapshot of what your business owns (assets), owes (liabilities), and what’s left over (equity) at a specific point in time. The foundational equation — assets equal liabilities plus equity — is what keeps this report balanced, literally.

Profitable on paper and broke in reality is a more common combination than most new business owners expect, especially under accrual accounting where revenue is recorded before cash actually arrives. The cash flow statement tracks the physical movement of money in and out, which is what actually determines whether you can make payroll next week.

1. Mixing personal and business expenses. Beyond the bookkeeping headache, commingling can undermine the liability protection an LLC or corporation is supposed to give you.

2. Misclassifying contractors and employees. Getting 1099 vs. W-2 status wrong isn’t a paperwork technicality — it carries real financial and legal consequences with the IRS.

3. Letting your paper trail go cold. No receipt, no proof — and no proof means no deduction if you’re ever audited. Most U.S. tax professionals recommend keeping supporting records for at least three to seven years, depending on the situation, so build a digital filing habit rather than trusting a shoebox (or its digital equivalent, the “Downloads” folder).

4. Skipping reconciliation. This is the step where errors, duplicate charges, and outright fraud get caught. Skip it for a few months and you’re not just behind — you’re bookkeeping blind.

How much do bookkeepers charge? Pricing varies widely by scope and service model. Basic software-supported plans can start in the low hundreds per month, while services that include a dedicated bookkeeper or controller oversight tend to run higher. Get quotes based on your actual transaction volume rather than relying on a single benchmark figure.

Can I do my own bookkeeping? Yes, especially in the early stages of a simple business — plenty of solo founders manage their own books using accounting software. The trade-off is time and risk: as transaction volume and complexity grow (payroll, inventory, multiple revenue streams), the hours it takes and the cost of a mistake both climb, which is usually the point where outsourcing starts to pay for itself.

What records do I need to keep for taxes? At minimum: bank and credit card statements, receipts and invoices for income and expenses, payroll records if you have employees, and documentation for any major purchases or contracts. Digital, organized, and backed up beats a shoebox every time — you’ve heard that from me twice now, and I mean it both times.

Good bookkeeping isn’t about becoming a numbers person overnight. It’s about building small, boring, repeatable habits — a weekly ten minutes here, a monthly reconciliation there — so that tax season stops being a crisis and starts being a formality. Consistency beats perfection every time.